Per Stirpes vs. Per Capita: A Small Beneficiary Choice That Can Change Everything

Most people assume their estate plan works like a master control panel: sign the will, fund the trust, and the right assets go to the right people. Charming theory. Real life is messier.

When it comes to retirement accounts, life insurance policies, and many annuities, the beneficiary designation often controls the outcome—not the will and not the trust unless the trust is specifically named. That is why the difference between per stirpes and per capita matters so much. A few words on a form can decide whether a deceased child’s share passes to that child’s children or is absorbed by surviving beneficiaries.

For Florida families, business owners, and professionals, this is exactly the kind of issue that should be reviewed with a Florida estate planning lawyer as part of a broader planning strategy. It also overlaps with conversations people often have with a Florida business attorney and a Florida asset protection attorney, especially when family wealth includes business interests, investment accounts, and real estate.

What does per stirpes mean?

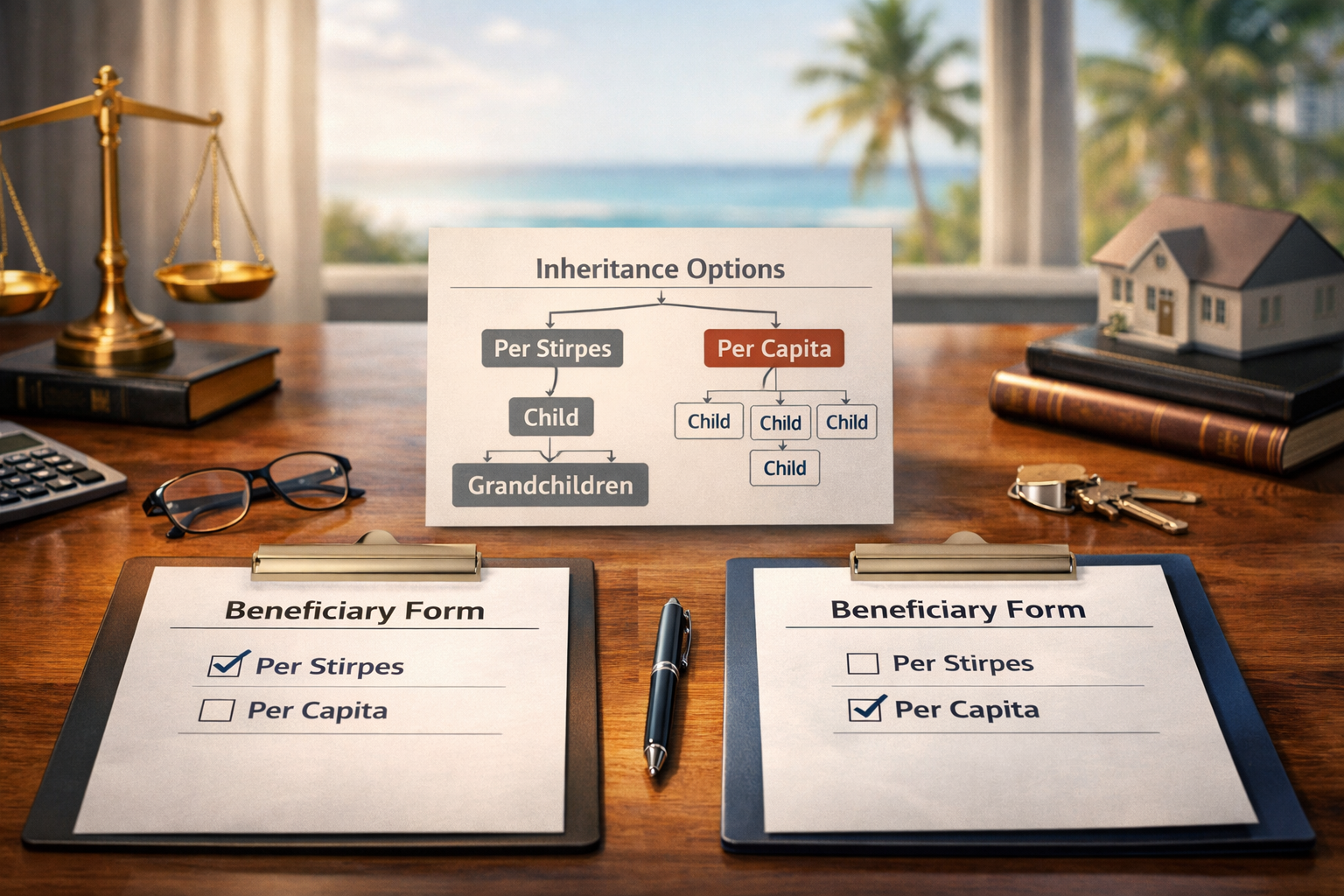

Per stirpes means “by branch.” If a named beneficiary dies before you, that beneficiary’s share generally passes to that person’s descendants instead of being reallocated to the surviving beneficiaries. Kiplinger’s example is simple: if two children are each named for 50%, and one dies before the parent, that deceased child’s 50% would go to that child’s own children.

In plain English: per stirpes keeps each child’s branch of the family in the inheritance line.

That can be exactly what a parent or grandparent wants, especially in blended families or families where one child dies young but leaves children behind.

What does per capita mean?

Per capita means “by head.” If one named beneficiary dies before you, that beneficiary’s share is generally divided among the surviving named beneficiaries. In the same two-child example, if one child dies first, the surviving child may receive 100% and the deceased child’s children may receive nothing.

That is not necessarily wrong. Some people want the surviving beneficiaries to take everything. But plenty of families choose that result accidentally because nobody explained the distinction and nobody reviewed the form.

Why this matters more than people realize

This issue matters because beneficiary designations often sit quietly outside the core estate-planning documents people focus on. Kiplinger emphasized that many families spend time on wills and trusts but never stop to examine the beneficiary forms tied to IRAs, 401(k)s, insurance policies, and annuities.

FINRA likewise explains that beneficiary designations on retirement accounts typically determine who inherits those assets, regardless of what the will or trust says. Fidelity’s materials also show that a per stirpes result usually must be chosen on the account paperwork rather than assumed.

That is the trap. Families think they have one unified plan, but in reality they may have:

- a will saying one thing,

- a trust saying another,

- and beneficiary forms saying something else entirely.

The hidden problem: custodian defaults

Here is where the paperwork gremlin really earns his paycheck: not every financial institution handles this the same way.

Kiplinger notes that some custodians default to per capita, some allow per stirpes only if requested, and some may not offer the option in every situation. Fidelity’s forms reinforce that per stirpes often must be specifically stated or selected.

That means silence is not neutral. Silence is a decision you may not realize you made.

A Florida planning angle

For Florida residents, this question often comes up in estate plans that also involve revocable trusts, family LLCs, business succession, and asset protection planning. If your plan is supposed to benefit children equally by family line, or if your grandchildren are intended backup beneficiaries, then your beneficiary designations need to match that goal.

This is especially important where the family wealth is not just a checking account. Think:

- IRAs and 401(k)s

- life insurance

- annuities

- closely held business interests

- entities used in Florida LLC and asset protection planning

- real estate held inside larger succession plans

A Florida estate planning lawyer can help coordinate the beneficiary forms with the trust, while a Florida asset protection attorney or Florida business attorney may help ensure the rest of the structure supports the same family objectives.

A practical example

Suppose a mother has two children, Alex and Brooke, each named as 50% beneficiaries of an IRA. Brooke dies before the mother, leaving two children.

If the IRA is per stirpes, Alex still gets 50%, and Brooke’s two children split Brooke’s 50%.

If the IRA is per capita, Alex may take 100%, and Brooke’s children get nothing.

Now add real life:

- one child had kids and the other did not,

- one child died after a divorce,

- one child is estranged,

- or a blended family has stepchildren and grandchildren in the picture.

Tiny language choice. Enormous human consequence.

When should beneficiary designations be reviewed?

- after a marriage or divorce,

- after the birth of a child or grandchild,

- after the death of a beneficiary,

- after opening a new retirement or brokerage account,

- and whenever your estate plan is updated.

Frequently asked questions

Does my will control my IRA?

Usually no. For most retirement accounts, the beneficiary designation controls unless the estate or trust is actually named as beneficiary.

Is per stirpes always better?

No. It depends on your goals. Per stirpes is often better when you want each child’s family line protected. Per capita may fit other family intentions.

Do all institutions offer the same options?

No. Custodian forms and defaults vary. That is why account-by-account review matters.

Can I just rely on my trust?

Not safely. If the trust is not the named beneficiary, the account may pass outside it. Even where a trust is named, tax and administration issues can become more complex. The IRS notes that special rules apply when a trust is named as beneficiary of a retirement account.

Final thought

Per stirpes vs. per capita sounds like the sort of Latin distinction people nod at during meetings while secretly planning lunch. But this one has teeth.

If you want your assets to follow family branches, protect grandchildren, and align with your broader estate plan, do not leave the answer to default settings buried in an old form. Review the paperwork. Align it with your intent. Then sleep better knowing your legacy is not being outsourced to administrative happenstance.